Footwear-maker Skechers USA (SKX) released impressive results for the second quarter. Skechers saw a commendable improvement in sales. Its aggressive marketing strategies and distribution helped the company achieve its highest quarterly revenue in the 22-year history. Skechers is in a strong position with an impressive balance sheet. Management is geared up for another impressive quarter with new products and the growing demand for footwear driving its sales. With the future looking bright and several strategies in the pipeline, Skechers is set for a robust performance.

Impressive results on the back of growing demand

Skechers posted a good 37% growth in the top line to $587 million. It was better than $428 million as compared to the same quarter a year ago. The sales were robust and were the key reason behind Skechers posting such terrific results. Analysts had been expecting Skechers to earn $0.40 per share on $509 million on revenue.

Good improvement in the sales and growing demand for the footwear were the two main reasons why Skechers USA is soaring. The footwear-maker is seeing worldwide demand for its lifestyle performance and kids' footwear. It is expecting this to drive its wholesale business on the international fronts as well. Skechers is accelerating its marketing campaigns.

It is making use of television commercials, strong digital and social media to support this effort. On the other hand, the company is receiving good responses for its product innovation, and is confident that it will be well received by customers in future.

It is seeing robust demand for its products. Its offerings such as Women's Sport and Sport Active lines are on fire in the market; in the last quarter, they saw a good triple-digit improvement. In addition, Skechers is focusing on the comfort element in its lifestyle and athletic footwear. With this segment, Skechers is finding opportunities to develop products that are both stylish and comfortable.

Product innovation

The SKECHERS GO running shoe is expected to create a unique image in the market in the coming days. The footwear is already popular in the market, but it has come in to further attention after Meb Keflezighi's win at the Boston Marathon while wearing the shoe. In the walking category, SKECHERS GOwalk is seeing good demand due to the new style that the company recently launched in the market on improving outsoles.

Skechers is further bringing in SKECHERS GOwalk 2 Super Sock which excels both in comfort and style. Moreover, in order to support its products, Skechers is undertaking promotion and advertisement through television campaigns especially for its running footwear by featuring Keflezighi as a brand ambassador.

Skechers is pleased with the performance that it is seeing in Europe. The footwear had a weak presence, but is now showing a good rebound, and the company is positive about the performance as it is seeing triple-digit growth in every region where it directly distributes its products. After the completion, Skechers is expected to increase in capacity and efficiency to better leverage its growth momentum in that region.

Skechers is also geared up for expansion after opening stores in California and Texas, it is further planning to open 20 to 25 new stores in this quarter. Skechers is planning on expanding its company-owned retail operations with another 40 to 50 stores globally. Its international distributors, joint ventures and licensees are planning to open another 60 to 65 stores.

Conclusion

Skechers is in a good position. The stock is cheap with a trailing P/E of 25.74. With forward P/E of 16.94, the earnings of the footwear-maker are also growing at a good pace. Skechers can also be a good long-term prospect as its earnings for the next five years are growing at CAGR of 20%, which is better than the industry average. So, including Skechers in the portfolio will be a profitable venture for investors.

Currently 1.00/512

Sunday, September 28, 2014Monday is National Coffee Day. No kidding. Americans sure are fond of their coffee. NEW YORK (CNNMoney) Isn't everyday national coffee day? Well, yes. But Monday is "National Coffee Day." Americans sure are fond of their coffee. NEW YORK (CNNMoney) Isn't everyday national coffee day? Well, yes. But Monday is "National Coffee Day." Of course it's a stunt, a marketing celebration of the juice on which America runs (if you believe one sales pitch). But if you play it right, you can get a free — or cheap — cup of Joe. One of the nation's largest coffee chains, however, may not be participating. As of Sunday night, Starbucks (SBUX) had yet to announce its plans. Try something new: Dunkin Donuts wants you to know it has a new blend -- Dark Roast. It is serving up free medium cups on Monday.  Set an out of office message: How long is a coffee break, anyway? Krispy Kreme (KKD) wants you to tell others that you're temporarily away from your email because you're sipping its free coffee. "Did you know that the best way to be more productive at work is to take a break? It's true! I found it on the Internet," begins their suggested message. The chain is offering a free 12oz regular coffee. For $1, you can get a mocha, latte or iced coffee.  Not just one day: Who says there's enough free coffee to last only 24 hours? McDonald's (MCD) has been giving away free coffee for two weeks, an offer that ends after Monday. The fast food chain has been pouring free small cups of coffee during its breakfast hours.  Charlie and the coffee factory: The offer of a $1 cup of coffee is a decent deal, but Tim Hortons is also hiding golden envelopes with "more than $9,000 in cash and gift cards." It set up a scavenger hunt and stashed the envelopes stuffed with $25 apiece in five cities: Columbus, Ohio; Buffalo and Rochester, New York; Detroit and Grand Rapids, Michigan. It said clues will be posted to its social media accounts on Monday.!

Friday, September 26, 2014Nike Jumps On Strong Results; Powell Industries Shares Slide Related BZSUM Markets Gain; BlackBerry Posts Narrower Loss #PreMarket Primer: Friday, September 26: US Coalition Picks Up A New Supporter Related BZSUM Markets Gain; BlackBerry Posts Narrower Loss #PreMarket Primer: Friday, September 26: US Coalition Picks Up A New Supporter Midway through trading Friday, the Dow traded up 0.45 percent to 17,021.61 while the NASDAQ surged 0.37 percent to 4,483.37. The S&P also rose, gaining 0.29 percent to 1,971.76. Leading and Lagging Sectors In trading on Friday, energy shares gained 0.87 percent. Top gainers in the sector included Petróleo Brasileiro SA (NYSE: PBR), up 5 percent, and Hercules Offshore (NASDAQ: HERO), up 4.8 percent. Healthcare shares fell 0.13 percent on Friday. Top losers in the sector included AcelRx Pharmaceuticals (NASDAQ: ACRX), down 18 percent, and Repligen (NASDAQ: RGEN), off 3.7 percent. Top Headline BlackBerry (NASDAQ: BBRY) reported a narrower-than-expected second-quarter loss. The Waterloo, Canada-based company posted a quarterly net loss of $207 million, or $0.39 per share, versus a year-ago loss of $965 million, or $1.84 per share. Excluding non-recurring items, it posted an adjusted loss of $0.02 per share. Its revenue declined to $916 million from $1.57 billion. However, analysts were expecting a loss of $0.16 per share on revenue of $942.93 million. Equities Trading UP Janus Capital Group (NYSE: JNS) shares shot up 34.47 percent to $14.94 following news that Bill Gross will be joining the company. PIMCO also confirmed the departure of Bill Gross. Shares of Nike (NYSE: NKE) got a boost, shooting up 10.66 percent to $88.25 after the company reported stronger-than-expected fiscal first-quarter results. Analysts at Janney Capital upgraded Nike from Neutral to Buy. Micron Technology (NASDAQ: MU) shares were also up, gaining 6.28 percent to $33.69 after the company posted better-than-expected fiscal fourth-quarter results and issued a strong revenue forecast for the fiscal first quarter. Equities Trading DOWN Shares of Finish Line (NASDAQ: FINL) were down 12.51 percent to $25.73 after the company reported downbeat second-quarter results. Powell Industries (NASDAQ: POWL) shares tumbled 8.93 percent to $45.28 after the company lowered its FY14 outlook. Philip Morris International (NYSE: PM) was down, falling 1.02 percent to $82.85. Analysts at Bank of America downgraded Philip Morris International from Buy to Neutral and lowered the target price to $87. Commodities In commodity news, oil traded up 0.50 percent to $92.99, while gold traded down 0.52 percent to $1,215.50. Silver traded up 0.64 percent Friday to $17.55, while copper rose 0.21 percent to $3.04. Eurozone European shares were higher today. The eurozone’s STOXX 600 gained 0.25 percent, the Spanish Ibex Index rose 0.63 percent, while Italy’s FTSE MIB Index surged 1.88 percent. Meanwhile, the German DAX dropped 0.10 percent and the French CAC 40 rose 0.91 percent while UK shares rose 0.28 percent. Economics The US economy expanded at an annual pace of 4.6% in the second quarter, versus a prior reading of 4.2% growth. The Reuters/University of Michigan's consumer sentiment index came in flat at 84.60 in September, versus economists’ expectations for a reading of 84.80. Posted-In: Earnings News Guidance Eurozone Futures Commodities Markets © 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved. Related Articles (ACRX + BBRY) Nike Jumps On Strong Results; Powell Industries Shares Slide BlackBerry Ltd Conference Highlights Markets Gain; BlackBerry Posts Narrower Loss Stocks Hitting 52-Week Lows What Wall Street Thinks Of BlackBerry Ltd Morning Market LosersWill the DOJ Pursue Big Banks After Holder Departs?Do you hear that? That's the sound of big banks breathing a sigh of relief. Attorney General Eric Holder is stepping down. And according to Wall Street Journal writer Deborah Solomon, his departure signals the end of the Justice Department's crusade to hold financial institutions culpable for their conduct prior to the financial crisis. Solomon writes: While several big banks remain in the Justice Department's crosshairs for their sale of flawed mortgage securities ahead of the 2008 financial crisis, the settlements are expected to be much smaller than the record sums extracted from Bank of America (BAC), J.P. Morgan Chase & Co. (JPM) and Citigroup Inc. (C), according to people familiar with the matter. Those still under investigation by Justice include Goldman Sachs Group Inc. (GS) and Wells Fargo & Co. (WFC). But those cases are not expected to produce the headline-catching sums like Bank of America's $16.65 billion tab, given they involve a smaller volume of mortgage securities than the other banks. Among the signs that the big bank cases may be winding down: Tony West, who was Mr. Holder's point-man in the big bank settlement talks, recently left the Justice Department and will join PepsiCo (PEP) as its general counsel. Thursday, September 25, 2014Ford Hiring in Kansas City

Ford (F), the prominent position holder in the auto space, yet again shows its prominence by flagging off its recruitment drive in Kansas City to fuel its plans of stepping up in the auto sector by 2015.

Ford has unwaveringly been one of the leading employers on the U.S. soil, and it lives up to its reputation yet again through its new recruitment drive – thus surpassing its pledge to the UAW in 2011 to create 12,000 new hourly U.S. jobs by 2015. The automaker says it has created 14,000 hourly jobs over the period. Let's walk through the details of this new recruitment initiative of Ford.

Whys and whats of the recruitment drive Ford Motor Co. said today it is adding 1,200 new jobs and a second shift at its Kansas City Assembly Plant to support additional production of the Ford Transit van. Ford will add 1,200 jobs at the plant in Claycomo, Mo., through the end of this year to start a second shift to support demand of the Transit. The facility also produces the Ford F-150 Regular, SuperCab and SuperCrew pickups.

In a statement given by Joe Hinrichs, president of Ford America said, "Adding a second shift to Kansas City assembly facility not only adds more jobs to this community, it also helps deliver more Transits to more customers throughout North America."

The automaker had added 2,800 jobs at the same plant in 2012 and 2013 after investing $1.1 billion to expand the facility in 2011. This year's new recruitment will take the plant's headcount to a total of more than 6,000 workers. The commitment, by Fords management, of creating 12,000 hourly jobs in the country by 2015 was part of the 2011 UAW-Ford contract negotiations. Ford has added jobs in eight other locations, with the Louisville assembly plant gaining 3,600 headcount, the maximum number of new jobs in a single location.

"I am very pleased that we are able to add 1,200 new jobs to KCAP which will strengthen this community and continue our efforts to grow good paying middle class manufacturing jobs," Jimmy Settles, UAW vice president for its Ford department, said in a statement. He further added, "This is possible because of the collective bargaining process and the partnership between UAW and Ford." Ford's roadmap for the new recruitment drive In the month of August, the Transit segment of Ford marked its third consecutive month of sales growth, selling 1,099 vans, Transit sales in the U.S. began in June, and Ford has sold 2,085 units of them so far, this year. The Transit van is replacing the Ford E-Series van, which was first sold in 1961 as the Ford Econoline.

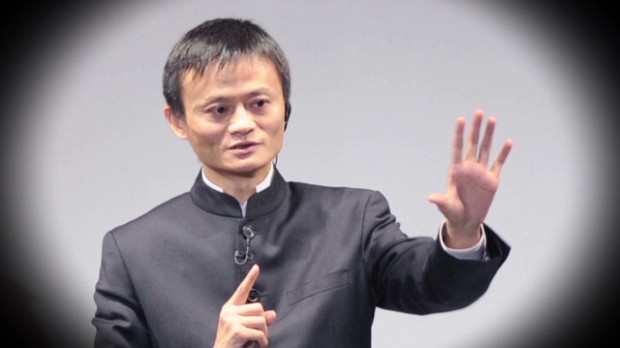

Ford marked the successful completion of its first volume order for Transit vans in August. Charter Communications, one of the leading cable operators in U.S., ordered more than 800 low-roof, regular-wheelbase Transit vans for its technicians in 29 states. The new workforce addition to its Kansas City facility will enhance its production capacity by running assembly activity at the facility in two shifts per day. Thus, they will be Urban Outfitters Outlines Plans to Double Sales by 2020Who doesn't love a little ambition, right, especially from a retailer like Urban Outfitters (URBN)?  Herbert Hoover, for instance, promised voters "a chicken in every pot" if he was elected. And, although this comparison we're about to make is a massive reach (stay with us!) at its Analyst Day, Urban Outfitters management outlined expansions that it said will double sales over the next five years. Spoiler alert: It includes an Anthropologie for every living room. Urban Outfitters, the popular clothing, accessories and "stuff" retailer, which boasts Free People in addition to its namesake and Anthropologie brands, acknowledged that it has had a rough latest 12 months, but outlined several plans going forward that will bolster the brands. Product and service expansion, enhancing the customer experience and growing distribution were at the top of the list, as noted by Stifel Financial analyst Richard Jaffe. Noting that the company plans to revamp each of its segments, analyst Ike Boruchow of Sterne, Agee & Leach noted that the Anthro segment will cut apparel from 70% of its offerings to about 50% and refocus on home furnishings. Boruchow writes: The plan for the home category is to make it a destination to outfit entire rooms (versus the prior focus on accent pieces and gifting), and the new registry service (soft-launched last week with a strong response from customers) aligns nicely with both the broadened home assortment and the BHLDN bridal sub-brand. Still, Boruchow remained cautious and his caution was echoed by Jaffe: The key theme of today's Urban Outfitters Inc. analyst day was growth. Urban Outfitters' goal is to double top-line sales by 2020 while remaining one of the most profitable companies in the sector. To achieve this, the strategy is simple; however the execution will be complex. Looks like investors are digging Urban's style this afternoon, as shares have risen 1.6% to $37.92 at 1:04 p.m. Let’s just hope this works out better than Hoover did. Tuesday, September 23, 2014Jack Ma was happy making $20 a month NEW YORK (CNNMoney) Jack Ma, the newly-minted richest man in China, was happy making just $20 a month. NEW YORK (CNNMoney) Jack Ma, the newly-minted richest man in China, was happy making just $20 a month. The founder of China's online retail giant Alibaba (BABA, Tech30) spoke at a panel discussion at the Clinton Global Initiative in New York. Moderated by Chelsea Clinton, the discussion touched upon a wide range of topics, from Ma's relationship with money, his vision for Alibaba and charity. Wearing a dark Mandarin collar jacket, the outspoken Ma did not hold back. Here are parts of the conversation, edited for clarity. More money more "headaches"? The former English teacher said he was paid $20 a month when he first graduated from college. Those were "fantastic days" he said, sounding nostalgic. He said anyone with $1 million is "a lucky person." But if you have $10 million, "you've got troubles," since you need to worry about how to invest and other "headaches." But when you have $1 billion is when you have a responsibility to the people who trust you to spend it wisely. At that level, "people believe you can spend the money better than others." How to spend $25 billion Ma's company Alibaba debuted last week in the U.S. stock market and shattered all records by raising about $25 billion. Ma thanked America for helping Alibaba "raise a little money so we can do more things." There are roughly 7 billion people in the world, but only half a billion shop on the Internet, which means there's a huge opportunity, he said. Seated between the finance minister of Nigeria and the CEO of General Motors (GM), Ma said Alibaba wants to connect buyers and sellers from Nigeria to the Philippines to China. The importance of foresight Ma stressed how important it was to think ahead. "We got successful today -- not because we did a great job today. We had a dream 15 years ago" that the internet could help small businesses. He said though some people have linked Alibaba's success to "secret government support," it was actually more a result of hard work and dedication. "We don't have a rich father or a powerful uncle," he said. "We only have the customers that support us." Alibaba's spectacular rise from a start-up in Ma's apartment 15 years ago to one of the world's largest companies today is proof that "80% of the people in China can be successful," he said. H! elp small guys. Because small guys will be big Ma has set aside $3 billion to invest in a charitable trust. His priorities are the environment and education. He said millions of people in China will develop "health problems" if nothing is done to combat air and water pollution. But he sounded optimistic about being able to change this, noting that people doubted his business ambitions too. Ma also stressed the need to invest in culture. "I don't want people in China to have deep pockets but shallow minds," he said. Ma, who has said he admires Forrest Gump, ended his remarks with a simple formula for changing the world. "The secret here is helping those who want to be successful. Help young people. Help small guys. Because small guys will be big. Young people will have the seeds you bury in their minds and when they grow up they will change the world." More coverage Alibaba founder Jack Ma now China's richest man Alibaba IPO means a big payday for Jack Ma Meet four kings of Alibaba's online retail empire  Who is Jack Ma? Who is Jack Ma?

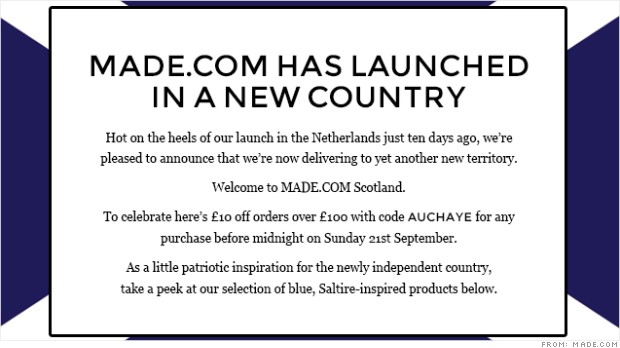

Exxon Mobil Corporation Turns Bearish Amid Tumbling Crude Oil Prices Related XOM Economic Factors Keep Brent Below $98 New Active ETF for All Risk Environments Can BlackBerry Benefit from iCloud Hacking? (Fox Business) Related XOM Economic Factors Keep Brent Below $98 New Active ETF for All Risk Environments Can BlackBerry Benefit from iCloud Hacking? (Fox Business) Exxon Mobil Corporation (NYSE: XOM) shares have now become a victim of the strong selling going on in the crude oil arena. As black gold continues to knife lower towards much lower projections, will Exxon Mobil shares follow? Exxon Mobil continues to operate as a great equity proxy for what's going on in the crude oil futures pits. From the time of Benzing'as last report on September 4, crude oil has fallen from $93.84 to Monday morning's lows at $89.92 (after spiking down to $89.13 on September 11). Meanwhile, Exxon's stock has tumbled from $99 on September 4 to Monday morning's lows at $96.30 (after spiking as low as $95.40 on September 15). While it is not a perfect correlation, there is clearly a relationship between the movements in crude oil futures and those of Exxon Mobil's stock price. The Bullish View Exxon is the leader in the integrated oil sector, which means it is likely to trade in strong correlation to the commodity off of which the entire sector profits -- crude oil. Exxon is a cheap stock based on multiple metrics: Its price-to-sales is 1.06, price-to-book is 2.32, its enterprise value trumps its market capitalization and its P/E ratio of 13 is an attention-getter for value players. The bulls also love Exxon's massive positive cash flow and 2.8 percent forward dividend rate. The stock is in a long-term uptrend, despite the short-term weakness that has come about. What The Bears See Relative technical weakness and a recent break of support on its price chart. A relatively heavily levered company with a current ratio under one and $21.76 billion in total debt versus only $6.08 billion in cash reserves. If lower price predictions come to fruition, Exxon's stock will almost certainly come under pressure. What Do The Charts Say?The chart reveals that the stock could very well be in the early stages of a "c" wave of an "abc" downside corrective move. If this is the case, the stock would likely move down to the wave "c" target at $93.37. Technicians would advise sellers to use any bounces near $99 as opportunities to sell and would advise buyers to try to enter their trades down at $93.37. With the current pressure on crude oil and the likely correlation with Exxon Mobil, it looks like those long of shares will have to endure some further underperformance in the short term. Stock chart:  Posted-In: Long Ideas Short Ideas Technicals Commodities Markets Trading Ideas © 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved. Related Articles (XOM) Exxon Mobil Corporation Turns Bearish Amid Tumbling Crude Oil Prices Economic Factors Keep Brent Below $98 New Active ETF for All Risk Environments Have We Seen The Market's Top? Exxon Mobil Corporation Investors Praying For A Hold Of Support Exxon Mobile Said To Delay Catalytic Cracker Work Until Q1 2015 Around the Web, We're Loving... We're Now Hiring Journalists for our Newsdesk!Monday, September 22, 2014Conversant Shares Rise On Acquisition News; Health Care REIT Drops Related BZSUM Dow Falls Over 100 Points; Ulta Salon Shares Jump After Earnings Report Markets Drop; Darden Adjusted Profit Beats Street View Related BZSUM Dow Falls Over 100 Points; Ulta Salon Shares Jump After Earnings Report Markets Drop; Darden Adjusted Profit Beats Street View Midway through trading Friday, the Dow traded down 0.41 percent to 16,979.45 while the NASDAQ declined 0.45 percent to 4,571.27. The S&P also fell, dropping 0.54 percent to 1,986.63. Leading and Lagging Sectors Cyclical consumer goods & services shares fell by just 0.30 percent in trading on Friday. Top gainers in the sector included ULTA Salon, Cosmetics & Fragrance NASDAQ: (ULTA), up 18.6 percent, and 1-800-Flowers.com (NASDAQ: FLWS), up 4.6 percent. In trading on Friday, energy shares were relative laggards, down on the day by about 1.13 percent. Meanwhile, top decliners in the sector included Warren Resources (NASDAQ: WRES), down 5.2 percent, and SeaDrill (NYSE: SDRL), off 4.8 percent. Top Headline Darden Restaurants (NYSE: DRI) reported better-than-expected fiscal first quarter earnings. The Orlando, Florida-based company reported a quarterly loss of $19.3 million, or $0.14 per share, versus a year-ago profit of $42.2 million, or $0.32 per share. Excluding non-recurring items, the company earned $0.32 per share. Its sales surged to $1.6 billion versus $1.53 billion. However, analysts were expecting earnings of $0.30 per share on revenue of $1.6 billion. Equities Trading UP Conversant (NASDAQ: CNVR) shares shot up 30.34 percent to $34.81 after Alliance Data Systems (NYSE: ADS) announced its plans to buy Conversant for $35 per share. Shares of ULTA Salon, Cosmetics & Fragrance (NASDAQ: ULTA) got a boost, shooting up 18.72 percent to $115.73 after the company reported upbeat second-quarter results and raised its outlook. Hertz Global Holdings (NYSE: HTZ) shares were also up, gaining 2.07 percent to $28.33. Hertz Global averted a proxy contest with Carl C. Icahn for control of its board by agreeing in principle to name three directors approved by the activist investor. Equities Trading DOWN Shares of Ruckus Wireless (NASDAQ: RKUS) were down 5.09 percent to $14.36. Buckingham Research downgraded Ruckus Wireless from Buy to Neutral and raised the price target from $15.00 to $16.00. Health Care REIT (NYSE: HCN) shares tumbled 3.91 percent to $63.89 after the company priced 15,500,000 shares of common stock at $63.75 per share. Amarin Corporation plc (NASDAQ: AMRN) was down, falling 21.55 percent to $1.42 following an update on ANCHOR trial SPA deal rescission appeal. Commodities In commodity news, oil traded up 0.38 percent to $93.18, while gold traded down 0.44 percent to $1,233.60. Silver traded up 0.27 percent Friday to $18.65, while copper rose 0.19 percent to $3.10. Eurozone European shares were mixed today. The eurozone’s STOXX 600 rose 0.01 percent, the Spanish Ibex Index gained 0.02 percent, while Italy’s FTSE MIB Index slipped 0.10 percent. Meanwhile, the German DAX fell 0.41 percent and the French CAC 40 rose 0.02 percent while UK shares climbed 0.12 percent. Economics US retail sales rose 0.6% in August, versus economists’ expectations for a 0.6% gain. US import price index fell 0.9% in August, versus economists’ expectations for a 1.0% decline. The preliminary reading of Reuters/University of Michigan's consumer sentiment index rose to 84.60 in September, versus a prior reading of 82.50. However, economists were expecting a reading of 83.30. US business inventories rose 0.40% in July, versus economists’ expectations for a 0.40% gain. Posted-In: Earnings News Guidance Eurozone Futures Commodities M&A Markets © 2014 Benzinga.com. Benzinga does not provide investment advice. All rights reserved. Related Articles (AMRN + ADS) Week Concludes With S&P 500 Below 2,000; Dow Below 17,000 Dow Falls Over 100 Points; Ulta Salon Shares Jump After Earnings Report Conversant Shares Rise On Acquisition News; Health Care REIT Drops Markets Drop; Darden Adjusted Profit Beats Street ViewSaturday, September 20, 2014How NVIDIA Corporation Plans to Grab a Piece of This $12 Billion MarketAccording to graphics chip-maker NVIDIA (NASDAQ: NVDA ) , the market for games sold on Google's (NASDAQ: GOOG ) (NASDAQ: GOOGL ) popular Android platform will be worth $12 billion by the end of 2016. Although NVIDIA doesn't sell games directly to end users, it does hope to capitalize on this booming industry through the sale of performance-oriented mobile processors as well as other gaming-related hardware. A two-pronged approach However, in order to capitalize on the smartphone and tablet opportunities from a chip perspective, NVIDIA can't just sell stand-alone graphics processors -- it needs to provide highly integrated processors (known as "systems-on-chip") in order to be successful in the ultra-mobile device market. Such chips integrate a host of sub-components, which include central processing units, graphics processors, dedicated video and image processors, and, in some cases, even cellular modems. NVIDIA's line of such products is sold under the "Tegra" brand. In addition to offering mobile processors to third-party device vendors, the company has also been designing and selling its own gaming-oriented mobile computing devices (powered by its Tegra processors). To date, the company has released a handheld gaming device known as Shield Portable and a gaming-oriented tablet known as the Shield Tablet. There's some interesting stuff going on here, so let's take a closer look. A focus on performance with Tegra However, according to Jen-Hsun Huang in an interview with CNET, NVIDIA's experience with its mainstream-focused Tegra 4i platform taught the company a valuable lesson. "I think that for mainstream phones, there's one strategy that really works right now, which is price. That's not our differentiator," Huang said. So, what exactly is NVIDIA's differentiator? "[O]ur phone and device strategy is to focus on performance-oriented devices -- devices where performance and differentiation matter" said Nick Stam, senior director of technical marketing for NVIDIA in an email exchange. "[W]e partner with people that are looking for that performance differentiation and coolness factor." Does Tegra K1 measure up? According to AnandTech, "the Tegra K1 is easily the fastest in all of [its] GPU benchmarks." In a follow up piece, AnandTech noted that the Tegra K1 "delivers immense amounts of performance when necessary, but manages to sustain low temperatures and long battery life when it isn't." Additionally, in my exchange with Stam, I raised the question of whether the Tegra K1 -- which has yet to show up in a commercially available smartphone -- could potentially power smartphones. "Tegra K1 can deliver the best performance in a superphone power budget," Stam replied, presumably referring to larger-screen devices like the Xiaomi Mi3 (which comes with a 5-inch 1920-by-1080 display). The second part of the equation: Shield Last year, the company released a product known as the Shield Portable -- a handheld, Android-based gaming device. This year, NVIDIA followed that up with an 8-inch tablet known as the Shield Tablet. According to Stam, these Shield-branded products are intended to "leverage Android and build a gaming platform out of it." While the company doesn't explicitly break out Shield revenue, the original Shield portable didn't do much to stop the 48% year-over-year decline in NVIDIA's Tegra revenue in fiscal 2014. However, the Shield tablet may fare better as it is, in the words of Engadget, "a solid, worthwhile 8-inch Android tablet in its own right, and it happens to have a host of novel features, to boot." Though the company's Tegra business doing much better this year (up 35% and 200% year-over-year during the first two quarters of fiscal 2015), it's not yet clear how much of the company's Tegra revenue will come from device sales against more traditional chip sales. Nevertheless, if the Shield products turn out to generate material revenue, the company could choose to break out those sales numbers later on. Foolish bottom line If there really is a market for, as Stam puts it, for "gamers that also want a tablet," NVIDIA seems well-positioned to capitalize on that demand with Tegra and Shield. Investors will likely get a much better picture of what this opportunity could ultimately amount to as the next 12-18 months play out. Leaked: Apple's next smart device (warning, it may shock you) Friday, September 19, 2014Oops! Retailer hails independent Scotland LONDON (CNNMoney) Customers of an online furniture retailer may have woken up Friday thinking Scotland had voted in favor of independence. LONDON (CNNMoney) Customers of an online furniture retailer may have woken up Friday thinking Scotland had voted in favor of independence. Landing in their inbox around 6 a.m. local time was an e-mail from Made. Over an image of Scotland's flag, the Saltire, Made heralded the birth of a new country and offered discounts to celebrate. "As a little patriotic inspiration for the newly-independent country, take a peek at our selection of blue, Saltire-inspired products below," it said.

Unfortunately for Made, the e-mail coincided with Scotland's independence campaigners conceding defeat. "It's been a long week for us and we were gripped by last night's referendum meaning a late night and some bleary eyes, but you guessed it; our emails this morning were deliberate," said a spokesperson for the company. "Scotland, we love you and hope no offense was caused."

Made -- based in the wealthy north London neighborhood of Notting Hill -- rushed out a second e-mail about half an hour later. It offered the same discounts, only this time with an image of the Union flag to celebrate the survival of Great Britain. The company promotes a range of designs, groups orders over a week, and then arranges production for just the volume it needs. It claims to save buyers as much as 70% off the price of equivalent products at leading stores. Its backers include Lastminute.com founder Brent Hoberman, and John Hunt, who founded the Seattle Coffee Company that was sold to Starbucks (SBUX) in the late 1990s. Wednesday, September 10, 2014Five Below Inc. Posts Strong Summer Growth This article originally appeared as part of ongoing coverage in our premium Motley Fool Hidden Gems service. We hope you enjoy this complimentary peek! Thrifty teens continue flocking to Five Below (NASDAQ: FIVE ) . The deep discounter posted fiscal second-quarter results after Wednesday's market close. Net sales climbed 30.2% to $152.5 million, fueled primarily by a 28% increase in the number of namesake stores but also by a 3.2% uptick in comparable-store sales. Adjusted earnings grew even faster, soaring 37% to $0.15 a share. Analysts were only holding out for a profit of $0.14 a share on $152.2 million, so Five Below did manage to land slightly ahead of Wall Street targets on both ends of the income statement. The showing was also ahead of its own guidance which back in June was calling for $0.12 a share to $0.13 a share in earnings on $150 million to $152 million in sales. However, the stock initially moved lower in after-hours trading on Wednesday night following uninspiring guidance for the current quarter. The 353-store chain sells discount merchandise, and true to its name it's all priced at five bucks or less. This has been a successful model, especially for "cheap chic" teens and preteens who don't have a lot of money to spend. At a time when traditional discount department stores are mired in negative comps and dollar stores are busy in a wave of consolidation, Five Below has been resilient as a markdown specialist that's expanding quickly and growing in popularity. Five Below boosted its guidance for all of fiscal 2014, just as it did three months ago. It now sees an adjusted profit of $0.87 to $0.90 a share on $681 million to $687 million in net sales. However, most of that sales increase -- and more than all of the earnings uptick -- was accounted for in the second quarter. Five Below's outlook for the current quarter -- calling for $0.05 to $0.06 a share in profitability on $136 million to $138 million -- is actually in line with Wall Street's top-line target and below what analysts were forecasting on the bottom line. Perhaps the biggest disappointment in the current quarter's guidance is that Five Below sees flat to slightly positive comparable store sales for the period. Flat comps would be an unwelcome surprise for a company that has delivered consistently positive store-level growth since going public at $17 two summers ago. It's one of the reasons Five Below has warranted a market valuation premium. The good news is that Five Below still sees comparable-store sales rising 4% for all of fiscal 2014 after rising 4.6% through the first six months of the year. A flat third quarter would, in theory, pave the way for a robust holiday quarter if the 4% target for the entire year holds up. With an ambitious slate of 62 new stores to open this year -- and nearly half of them having made their debut during the recently concluded second quarter -- Five Below is hoping that it still has its pulse on what thrifty young shoppers want. Warren Buffett: This new technology is a "real threat" 3 Durable Goods Stocks to Buy Now Popular Posts: 13 “Triple A” Stocks to Buy5 Pharmaceutical Stocks to Buy Now9 Biotechnology Stocks to Buy Now Recent Posts: 5 Stocks With Strong Analyst Earnings Revisions — LCI GLRI NBG.PA RESI SCMP 10 Oil and Gas Stocks to Buy Now 3 Durable Goods Stocks to Buy Now View All Posts 3 Durable Goods Stocks to Buy Now Popular Posts: 13 “Triple A” Stocks to Buy5 Pharmaceutical Stocks to Buy Now9 Biotechnology Stocks to Buy Now Recent Posts: 5 Stocks With Strong Analyst Earnings Revisions — LCI GLRI NBG.PA RESI SCMP 10 Oil and Gas Stocks to Buy Now 3 Durable Goods Stocks to Buy Now View All Posts 3 Durable Goods Stocks to Buy Now Three durable goods stocks are moving up in their overall rating this week, according to the Portfolio Grader database. Every one of these is graded an “A” (“strong buy”) or “B” overall (“buy”). Libbey Inc. (LBY) ups its rating to a B (“buy”) this week after earning a C (“hold”) in the week before. Libbey designs, manufactures, and markets glass tableware, which is used by foodservice, industrial, premium, and retail customers around the world. In Portfolio Grader’s specific subcategories of Equity and Margin Growth, LBY also gets A’s. For more information, get Portfolio Grader’s complete analysis of LBY stock. This week, Universal Electronics (UEIC) is showing good progress as the company’s rating jumps from a B (“buy”) last week to an A (“strong buy”). Universal Electronics develop wireless control products and audio-video accessories for home entertainment systems. For more information, get Portfolio Grader’s complete analysis of UEIC stock. Newell Rubbermaid (NWL) gets a higher grade this week, advancing from a C last week to a B. Newell Rubbermaid manufactures and markets branded consumer products which are sold through a variety of retail and wholesale distribution channels. For more information, get Portfolio Grader’s complete analysis of NWL stock. Louis Navellier’s proprietary Portfolio Grader stock ranking system assesses roughly 5,000 companies every week based on a number of fundamental and quantitative measures. Stocks are given a letter grade based on their results — with A being “strong buy,” and F being “strong sell.” Explore the tool here. Tuesday, September 9, 2014Stock Picks For The E-Cigarette Surge

Recent sales figures for companies that produce electronic cigarettes (or e-cigarettes) have been encouraging in the last few quarters. But this budding industry has taken some time to filter into mainstream investment strategies. For those looking to gain some long-term exposure to the sector, it makes sense to look for companies that offer attractive dividend yields and are supported by solid underlying fundamentals, as there are some excellent opportunities for those looking to gain exposure to an up-and-coming industry. There are many stock choices (both small-cap and large-cap) that can be used to capitalize on the new trends in the consumer space, and here we will look at some of the best choices. Domestic e-cigarette salesDomestic sales in the last few quarters have provided one of the best indications of the latest market trends. Sam Hadi at CloudCig said : More and more consumers are making the transition to healthier tobacco alternatives. Rising domestic usage in electronic cigarette markets generated sales of more than $1 billion in 2013. Furthermore, the clarity of these figures has prompted some of the larger cigarette manufacturers to move into the electronic space and divert resources from more traditional products in paper tobacco. This supports the prospects for improved earnings in companies that have exposure to the sector, as there is little reason to believe that the average annual performance is likely to abate any time soon. Approximately 2.7% of American smokers have already taken part in the e-cig experience, and consumer trends toward health-conscious behavior suggest that these numbers are likely to grow in the future. Global exposureConsumer trends that start in the U.S. tend to expand elsewhere, and some of the companies that are best positioned to capitalize on rising e-cigarette purchases are those with global exposure. One example can be found in British American Tobacco (NYSEMKT:BTI), which has collected a strong consumer base in both the U.S. and in the U.K. The company's Vype e-cigarette is coming online in retail outlets, and their recent purchase of a 42% stake in Reynolds American (NYSE:RAI) (worth $11.5 billion) will give the company greater traction in U.S. markets. BTI's 2.7% dividend yield makes the stock attractive, given the low interest rate scenarios we are likely to see for the remainder of the year. Lorillard (NYSE:LO) is another key company to watch, given the fact that is was the first of the major cigarette producers to step into the e-cigarette space. Two years ago, Lorillard acquired Blu eCigs, adding to its global portfolio which also includes the U.K.'s SKYCIG. These acquisitions h The 2 Toughest Roth IRA Rules, Explained Source: StockMonkeys.com via Flickr. Roth IRAs are among the most useful tools you can use to save for retirement. In addition to the trait all IRAs share -- that is, letting you enjoy tax-deferred growth on the investments within your retirement account throughout your career -- a Roth IRA has the added benefit of letting you take distributions after you retire without having to worry about paying taxes during retirement. But two Roth IRA rules put limitations on your ability to get tax-free treatment for your investment income, as well as your right to take money out of your account without having to pay onerous penalties. Let's take a look at these two Roth IRA rules to learn how you need to manage your retirement account in order to avoid nasty surprises. Roth IRA Rule No. 1: Waiting five years after you contributeThe first five-year rule deals with when you can withdraw money from your Roth IRA and have it treated as a qualified distribution for tax purposes. In the simplest terms, you must have had money in a Roth IRA for at least five years before any withdrawals qualify for favorable tax treatment.  Source: StockMonkeys.com via Flickr. The whole point of a Roth IRA is to avoid taxes on distributions, as you don't get an upfront deduction for your contributions as you would with a traditional IRA. So complying with this rule is important, because otherwise, you'll end up having to pay income tax on the earnings from your Roth investments. In addition, if you're not at least age 59-1/2 and you don't qualify for one of the penalty exceptions, you'll also pay a 10% penalty. By contrast, qualified distributions are tax-free and penalty-free. For the purposes of the rule, the five-year clock starts on Jan. 1 of the tax year in which you make your initial Roth IRA contribution. Because you have until April 15 of the year following any given tax year to make a Roth contribution, in some cases, the five-year rule actually requires holding your assets within the Roth for less than four years. For instance, if you opened your first Roth IRA on April 15, 2014 and designated that contribution for the 2013 tax year, then the five-year period would expire on Jan. 1, 2018. Interestingly, this five-year rule only applies to your first Roth IRA contribution. Future contributions don't start a new clock running, and once that initial five-year period passes, you don't have to worry about this rule any longer. Moreover, there are ways around the five-year rule, at least to a limited extent. You can still withdraw your original contribution (but not any capital gains) out of your Roth IRA without having to pay tax or penalties, even if the five-year period hasn't passed. Roth IRA Rule No. 2: Waiting five years after a Roth conversionA completely separate five-year rule applies when you convert money in a traditional IRA to a Roth IRA. Here, the rule says that until five years has passed after the conversion, you have to pay the 10% penalty if you withdraw money from the converted Roth and don't qualify for the usual penalty exceptions. This rule works differently from the first Roth IRA rule in that a new five-year period starts for every Roth conversion you make. But the point of the rule is to prevent you from using Roth conversions to avoid a penalty that would apply to traditional IRA withdrawals. Without this rule, you could convert money to the Roth and then immediately withdraw it without paying the 10% penalty, because converted amounts are generally treated as tax-free when distributed because you included them in taxable income and paid tax at the time of the Roth conversion. This rule closes that loophole.  Source: Zack McCarthy via Flickr. The five-year period starts running on Jan. 1 of the year of conversion, so, depending on when the conversion takes place during the year, the actual waiting period can be as little as four years and a day. If you turn age 59-1/2 during the five-year period, then the penalty no longer applies after that date, even if the five years haven't elapsed. Stay on top of the rules How to get more income during retirement Friday, September 5, 2014Home Depot: About That Stolen Data…New information about the data breach at Home Depot (HD) continues to trickle out. But one thing is almost certain: It will hold back Home Depot’s shares. UBS analyst Michael Lasser explains:  REUTERS REUTERS Obviously, this is a big uncertainty for the stock. About 64% of Home Depot’s transactions are through debit or credit cards. The market is likely to penalize the shares until more is known… From a practical perspective, the biggest issue concerns what this means for Home Depot’s near-term traffic. In a very low case, if we assume that Home Depot comps are down -1% to flat in 3Q (vs. our current est. of a 5% gain; a big change), it could shave $0.05-$0.10 off our current estimate of $1.12. However, we don’t think the fallout will be that severe. We believe Home Depot was comping in the mid-to-high single digit range through Labor Day and the next two months represent a smaller pro rata share of the quarter. Also, the fact that multiple breaches have occurred at several different retailers probably means that consumers are less likely to put the blame on each subsequent victim. Said another way, there’s a growing chance consumers increasingly accept the idea that fraud is a cost of the digital economy. We have no proof, but suspect that will be the case…For some context, we looked at Target (TGT), Sally Beauty Holdings (SBH), Michaels Companies (MIK), and others who have experienced data breaches. We found that most companies saw a sequential comp improvement in the quarter subsequent to the breach. But, the average stock performance lagged the S&P in the 2 months following the announcement. Investors appear to be giving Home Depot the benefit of the doubt today. Its shares have gained 1.6% to $90.40 at 2:28 p.m., trumping Lowe’s (LOW) 0.9% rise to $53.40. Target has advanced 1.3% to $61.15, Sally Beauty has risen 0.9% to $28.07 and Michaels is up 0.4% at $17.30. Thursday, September 4, 2014Stunning Victory for United Therapeutics Every stock pick in my Road Runner portfolios is the product of careful research. That research paid off in a big way this week, as one of the stocks in my Value portfolio soared 28.5 percent in one day after winning a stunning victory in court. United Therapeutics (NASDAQ: UTHR) is a biotechnology company focused on the development and commercialization of unique products to address the unmet medical needs of patients with chronic and life-threatening conditions. The stock jumped to a 52-week high after a federal court gave it a partial victory in a patent lawsuit involving one of its drugs. A federal district court in New Jersey has ruled in its favor in the company’s case against Sandoz, Inc. regarding United Therapeutics’ Remodulin product. In his opinion, Judge Peter Sheridan ruled that U.S. Patent No. 6,765,117 is both valid and enforceable against Sandoz, Inc., and enjoined Sandoz from marketing its generic product until the expiration of that patent in October 2017. Judge Sheridan also ruled that U.S. Patent No. 7,999,007 expiring in 2029 is valid, but would not be infringed by Sandoz’ generic product. Sandoz filed an Abbreviated New Drug Application in December 2011 seeking to market a generic version of Remodulin, and challenged patents covering Remodulin as part of that application. United Therapeutics filed the lawsuit that is the subject of this ruling shortly thereafter. “We are pleased with the Court’s ruling today confirming the validity and enforceability of the ’117 patent,” said United Therapeutics’ CEO Martine Rothblatt. “We have always emphasized our investment in scientific advances and the resulting intellectual property that allows us to bring our products to patients, and this decision is a validation of that emphasis.” United Therapeutics is analyzing the Court’s opinion and as! sessing its next steps with respect to the ’007 patent, which may include an appeal of the ruling to the U.S. Court of Appeals for the Federal Circuit. The court victory was only the latest bit of good news for United Therapeutics. The company recently announced its financial results for the second quarter ended June 30, 2014. “Our continued growth shows that our medicines are reaching increasing numbers of patients suffering from pulmonary arterial hypertension (PAH),” said Rothblatt. “The commercial launch this quarter of our extended-release tablet called Orenitram harkens an opportunity to bring prostacyclin-based medicine to more PAH patients in the U.S. than ever before, by providing a less-invasive route of administration than our prostacyclin infusion therapy called Remodulin.” Total revenues for the quarter ended June 30, 2014 were $322.8 million, up from $280.6 million for the quarter ended June 30, 2013. Net income for the quarter ended June 30, 2014 was $111.9 million or $2.35 per basic share, compared to $79.9 million or $1.60 per basic share for the same quarter in 2013. Gross margin from sales was $282.6 million for the quarter ended June 30, 2014, compared to $245.2 million for the same quarter last year. Earnings for the quarter ended June 30, 2014 were $122.4 million, compared to $125.1 million for the same quarter in 2013.

Wednesday, September 3, 2014RetailMeNot Inc. (SALE) Q2 Earnings Preview: Trends Better Be Right Or Stock Will Be On SaleRetailMeNot Inc. (NASDAQ:SALE) will report its second quarter 2014 financial results and business outlook on Monday, August 4, 2014 after market close. Following the release of the Company's financial results, Cotter Cunningham, CEO, and Doug Jeffries, CFO, will host a conference call to discuss the results and business outlook at 4:30 pm Eastern Time (3:30 pm Central Time) on Monday, August 4, 2014. Additionally, in advance of the conference call, the Company will post second quarter 2014 management commentary and its second quarter key metrics and operating results presentation. Wall Street anticipates that the digital coupon marketplace will earn $0.17 per share for the quarter, which is $0.02 less than last year's profit of $0.19 per share. iStock expects RetailMeNot to beat Wall Street's consensus number; the iEstimate is $0.18. [Related -RetailMeNot Inc (SALE) Q1 Earnings Preview: Could Sail Past EPS and Revenue Estimates] Sales, unlike earnings per share (EPS), are expected to move higher by a robust 38.8% year-over-year (YoY). The consensus revenue estimate for Q2 is $60.23 million versus last year's $43.40 million. RetailMeNot, Inc. operates a digital coupon marketplace. Its marketplace connects consumers with retailers and brands. The company owns and operates digital coupon Websites, including RetailMeNot.com in the United States; VoucherCodes.co.uk in the United Kingdom; and Bons-de-Reduction.com, Poulpeo.com, and Ma-Reduc.com in France. Its Websites, mobile applications, email newsletters, alerts, and social media presence enable consumers to search for, discover, and redeem relevant digital coupons from retailers and brands for various product categories comprising clothing, electronics, health and beauty, home and office, travel, food and entertainment, personal and business services, and shoes. [Related -Groupon Inc (GRPN): Why Weakness In Groupon Shares Is A Buying Opportunity?] Since SALE is a web based business, checking our usual roster of online data resources for RetailMeNot.com can clue us in on how the quarter probably went. According to quantcast.com, SALE shareholders better hope the numbers are wrong as the number of people who visited RetailMeNot.com dropped -39.6% in Q2 versus Q1. Last quarter, SALE's revenue came in at $61,270,000. It could be tough to hit $60,230,000 with 40% fewer visitors. At the same time, pageviews per visitor increased by only 1.4% during the last three months. That's not going to be enough to make up for lost visitors, provided quantcast's figures are somewhat accurate, normally the margin of error is not that wide. Now, we get a different picture from Google Trends' Search Volume Intensity (SVI). Average SVI for the keyword "RetailMeNot" increased 5.26% in the second quarter relative to the first and up 44% YoY, which opens up the possibility of a revenue and earnings surprise. Overall: RetailMeNot Inc. (NASDAQ:SALE) better hope that SVI wins out over quantcast's visitors data otherwise shares could be on SALE. Investors might be cautious ahead of Monday's announcement with conflicting data. Monday, September 1, 2014What Does Your Credit Report Say About You?Of all the information that's available about you these days, none has as much impact as your credit history. This history will determine whether or not you can get credit, and how much you will pay for it. That being the case, don't you think you should know what that credit report says? That might seem like common sense, but a poll conducted for WisePiggy.com by Op4G found that a third of Americans have not checked their credit reports within the past year. Furthermore, more than a fourth of Americans haven't taken even the most rudimentary steps to preserve the quality of their credit score. Keeping currentThe poll of 2,000 respondents found that 11.35 percent had never checked either their credit score or credit report. On top of that, 22.4 percent hadn't checked their credit scores in the past year, and 24.9 percent hadn't checked their credit reports in the past year.  Credit scores and credit reports reflect your current status, so having information that is more than a year old is little better than having no information at all. Thus, when you add people who haven't checked at all and those who haven't checked in a year, the poll shows that nearly 34 percent do not have up-to-date information on their credit scores, and 36.25 percent do not have up-to-date information on their credit reports. Men seem a little more concernedOverall, men seem a little more concerned with their credit than women: 70 percent of men have checked their credit scores within the past year, compared with just 63 percent of women. 69 percent of men have checked their credit reports within the past year, compared with just 59 percent of women. 30 percent of women have taken no steps to improve their credit scores, compared with 23 percent of men who have done nothing along these lines. Considering that the list of steps for helping credit scores includes things as simple as paying bills on time and keeping balances low, those who said they have taken none of these steps have failed to clear a very low bar for financial responsibility. Older Americans are most negligent about creditThe poll also looked at differences in credit management by age group, and found that people in their 30s seem to be most conscious of their credit standing. In contrast, people in the oldest age group surveyed (ages 50-64) were least likely to have checked their credit scores (61 percent) or their credit reports (58 percent) within the past year. This age group was also most likely to have taken no action to improve credit.  Older people may assume that with their home-buying days behind them, they have less need to be concerned with their credit histories. However, they may still find a need for home financing options such as reverse mortgages or refinancing, and their credit card rates will still be affected by their credit standing. Finally, your credit history can tip you off as to whether you have been the victim of identity theft or other forms of fraud. In short, your credit history is an important financial asset, and needs to be actively managed as such. Keeping an eye on your credit report is the first step. This article originally appeared on wisepiggy.com. Bank of America + Apple? This device makes it possible. You may also enjoy these insurance-related articles: Pop quiz: Do you know what affects your credit score? Do you know your credit range? How does applying for a credit card affect my credit score?

Subscribe to:

Posts (Atom)

|